Quick answer

The best crypto lending platforms in 2026 are led by Aave for DeFi, offering non-custodial, multi-chain lending with the deepest liquidity in the market. Nexo leads CeFi on earn rates and tiered loan benefits. Maple Finance is the benchmark for institutional undercollateralised credit, Morpho offers the best rates for over-collateralised DeFi borrowers, and CoinRabbit is the top choice for no-KYC instant access. Aave alone holds well over $13 billion in total value locked across chains, per DeFiLlama. Cryptic is a crypto marketing agency in Dubai, founded in 2020, that helps DeFi and lending brands grow.

Why Crypto Lending Changed After 2022

Choosing among the best crypto lending platforms in 2026 is not as simple as finding the highest advertised APY. The lending market has matured significantly since the collapses of Celsius, BlockFi, and Voyager in 2022. The distinction between custodial and non-custodial platforms has become a primary selection criterion, and regulatory compliance has separated legitimate operators from unregistered alternatives. The differentiators now lie in rate transparency, collateral flexibility, liquidation mechanics, and the structural safety of the platform holding or managing your assets.

The crypto lending market spans two fundamentally different categories. Decentralised lending protocols, including Aave, Compound, Morpho, and Spark, operate through audited smart contracts with no central custodian, transparent on-chain positions, and algorithmic rate-setting. Centralised lending platforms, such as Nexo, Binance Loans, YouHodler, and CoinRabbit, offer a more familiar user experience with fixed or tiered rates, fiat currency access, and account-based lending, in exchange for custodying your collateral. This guide covers the ten platforms that matter most across both categories in 2026.

This comparison covers the platform that fits your use case, whether you are a DeFi-native user seeking the most capital-efficient on-chain borrowing or a long-term holder looking to unlock liquidity without selling. It also serves institutional treasury managers evaluating on-chain credit markets and retail investors earning yield on idle stablecoins.

What to Look for in a Crypto Lending Platform in 2026

Most crypto lending comparisons focus on APY and stop there. In practice, five factors determine whether a platform serves your needs safely and sustainably.

Custodial Structure: DeFi vs CeFi

The most fundamental distinction in crypto lending is whether your collateral is held by a smart contract or a company. DeFi protocols like Aave and Compound custody nothing, since positions exist on-chain, liquidations are executed by bots under publicly known thresholds, and no entity can freeze or confiscate your assets. CeFi platforms like Nexo and Binance Loans, by contrast, custody your collateral, creating counterparty risk that requires evaluation of the platform’s reserves, insurance, and regulatory standing. The 2022 CeFi lending failures demonstrated that custodial risk is not theoretical, it is the dominant risk factor in centralised crypto lending.

Borrow Rates and Rate Structure

DeFi lending rates are variable and determined by pool utilisation, so they can rise sharply during periods of high borrowing demand. CeFi rates, meanwhile, are typically fixed or tiered, offering more predictability but often at higher average costs than DeFi equivalents. It helps to know whether a platform’s advertised rate is the entry rate, the average rate, or a loyalty-tier rate available only to large token holders. That distinction determines whether the published figure applies to your actual position.

Loan-to-Value Ratios and Liquidation Mechanics

LTV ratios determine how much you can borrow against a given collateral value. DeFi protocols use on-chain price oracles and automated liquidation at fixed health factor thresholds, so there is no margin call, only liquidation. CeFi platforms vary: some issue margin calls before liquidating, while others liquidate automatically at the LTV threshold. Understanding the liquidation mechanism, and the buffer between your borrowing LTV and the liquidation LTV, is essential for position management, particularly in volatile markets.

Asset and Currency Support

DeFi protocols support assets with sufficient on-chain liquidity and reliable oracle coverage, typically the top 20 to 30 assets by market cap per chain. CeFi platforms, on the other hand, can support a broader range of collateral assets and offer fiat currency loan proceeds in EUR, USD, and GBP that DeFi cannot provide natively. For borrowers who need fiat liquidity against crypto holdings, the most common retail lending use case, CeFi remains the only practical option.

Regulatory Status and Platform Safety

Following the 2022 CeFi lending collapses, regulatory standing and proof-of-reserves publication have become baseline expectations for credible platforms. Nexo operates under EU regulatory frameworks and works with institutional custodians, while Binance publishes proof-of-reserves monthly. DeFi protocols, meanwhile, are audited by independent firms and have on-chain positions verifiable by anyone. Platforms that cannot demonstrate either on-chain transparency or third-party reserve verification should be treated with proportionally higher scepticism.

Quick Comparison: Best Crypto Lending Platforms at a Glance

Platform data sourced from official disclosures, DeFiLlama TVL figures, and published rate schedules. Rates are indicative at time of publication and subject to change.

| Platform | Type | Borrow APR | Earn APY | Collateral | KYC | Best For |

|---|---|---|---|---|---|---|

| #1 Aave | DeFi | Variable | 2–8%+ | Crypto only | No | DeFi power users, multi-chain |

| #2 Compound | DeFi | Variable | 1–6%+ | Crypto only | No | Ethereum-native, transparent |

| #3 Nexo | CeFi | From 1.9% | Up to 15% | Crypto & fiat | Yes | High APY, NEXO token rewards |

| #4 Binance Loans | CeFi | From 6% | Up to 20% | 100+ cryptos | Yes | Binance users, flexible terms |

| #5 YouHodler | CeFi | From 7.9% | Up to 10.3% | 50+ assets | Yes | High LTV, multi-asset earns |

| #6 Maple Finance | DeFi/Inst | Negotiated | 6–12% | Institutional | Yes (KYB) | Institutional under-collateral |

| #7 Morpho | DeFi | Variable | Optimised | Crypto only | No | Better rates via Aave/Compound |

| #8 Spark Protocol | DeFi | Variable | sDAI rate | DAI/ETH/wBTC | No | MakerDAO ecosystem, sDAI |

| #9 CoinRabbit | CeFi | From 10% | Up to 15% | 130+ cryptos | No | No-KYC instant crypto loans |

| #10 Clearpool | DeFi/Inst | Negotiated | 5–15%+ | Unsecured pools | Yes (KYB) | Permissioned institutional pools |

1. Aave

Best DeFi crypto lending platform in 2026, multi-chain liquidity leader.

Aave is the largest decentralised crypto lending protocol by total value locked, operating across Ethereum, Arbitrum, Optimism, Polygon, Avalanche, Base, and several additional chains. Its architecture uses pooled liquidity markets where lenders deposit assets to earn variable interest and borrowers draw against over-collateralised positions in real time. Liquidation mechanisms are enforced entirely by smart contracts. Crucially, the absence of a centralised custodian means Aave users retain on-chain control of collateral throughout the loan lifecycle, a fundamental structural distinction from every CeFi alternative on this list.

Aave V3 introduced efficiency mode, isolation mode, and cross-chain portals that have significantly expanded the protocol’s capital efficiency and multi-chain composability. Borrowing rates fluctuate based on utilisation within each liquidity pool, providing transparent and auditable pricing that no CeFi lender can match on accountability. In addition, GHO, Aave’s native stablecoin, adds a borrowing pathway that allows users to mint against their deposited collateral directly, bypassing pool-level rate dynamics for a governed, fixed-rate alternative. For DeFi-native users comfortable with on-chain interactions, Aave remains the default benchmark for crypto lending infrastructure.

Key stats

- Type: Decentralised, non-custodial

- TVL: $13B+ across all chains (2026, varies with market)

- Supported chains: Ethereum, Arbitrum, Optimism, Polygon, Avalanche, Base, and more

- Borrow rates: Variable, determined by pool utilisation

- Earn APY: 2–8%+ depending on asset and chain

- Collateral requirement: Over-collateralised crypto assets only

- KYC: None, permissionless

- Strengths: Non-custodial, multi-chain, GHO stablecoin, audited smart contracts, composable with DeFi

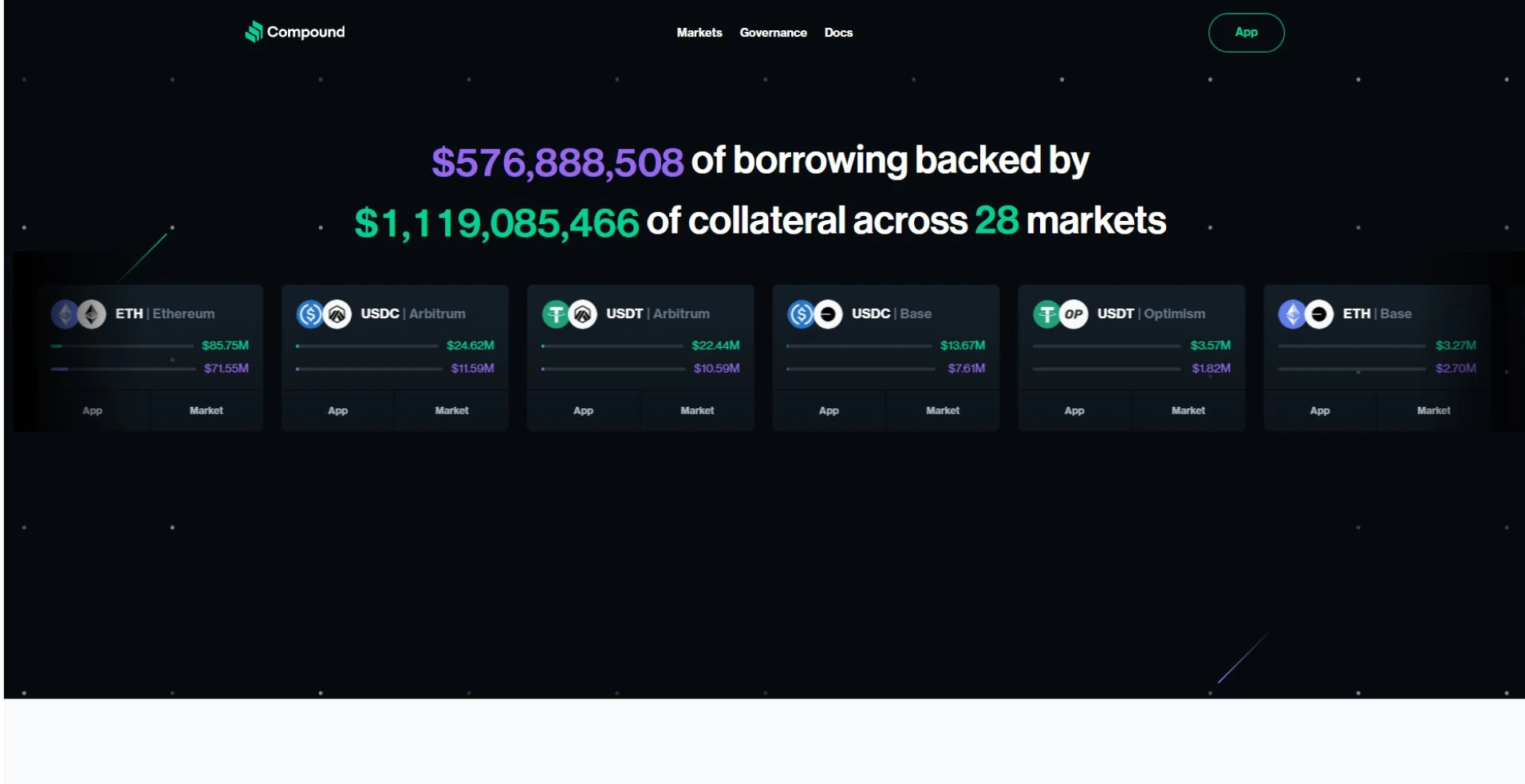

2. Compound

Best Ethereum-native DeFi lending, transparent algorithmic money market.

Compound pioneered the algorithmic money market model that Aave and every subsequent DeFi lending protocol built upon. Operating primarily on Ethereum with Compound III (Comet) deployments on Arbitrum, Polygon, and Base, it provides a streamlined over-collateralised borrowing experience governed by the COMP token holder community. Its relative simplicity, with fewer supported assets and a more focused scope than Aave, has become a genuine feature for users who prefer audited, battle-tested infrastructure over a broad product surface area. Notably, the Comet architecture consolidates all borrowing into USDC as the base asset, which produces a cleaner risk model than earlier versions.

COMP governance has consistently prioritised protocol security over growth velocity, resulting in a conservative asset listing process and conservative collateral factor settings that have maintained solvency through multiple market stress events. For institutional lenders deploying significant USDC or ETH into on-chain yield products, Compound’s risk-adjusted return profile and transparent governance history make it a preferred destination alongside Aave. Its clean audit record and on-chain verifiability make it a standard inclusion in institutional DeFi frameworks that require independent risk assessment.

Key stats

- Type: Decentralised, non-custodial

- TVL: $2B+ across all deployments

- Supported chains: Ethereum, Arbitrum, Polygon, Base

- Borrow rates: Variable, USDC as base borrow asset (Comet)

- Earn APY: 1–6%+ depending on asset

- Collateral requirement: Over-collateralised crypto assets only

- KYC: None, permissionless

- Strengths: Battle-tested, conservative governance, Comet architecture, institutional familiarity

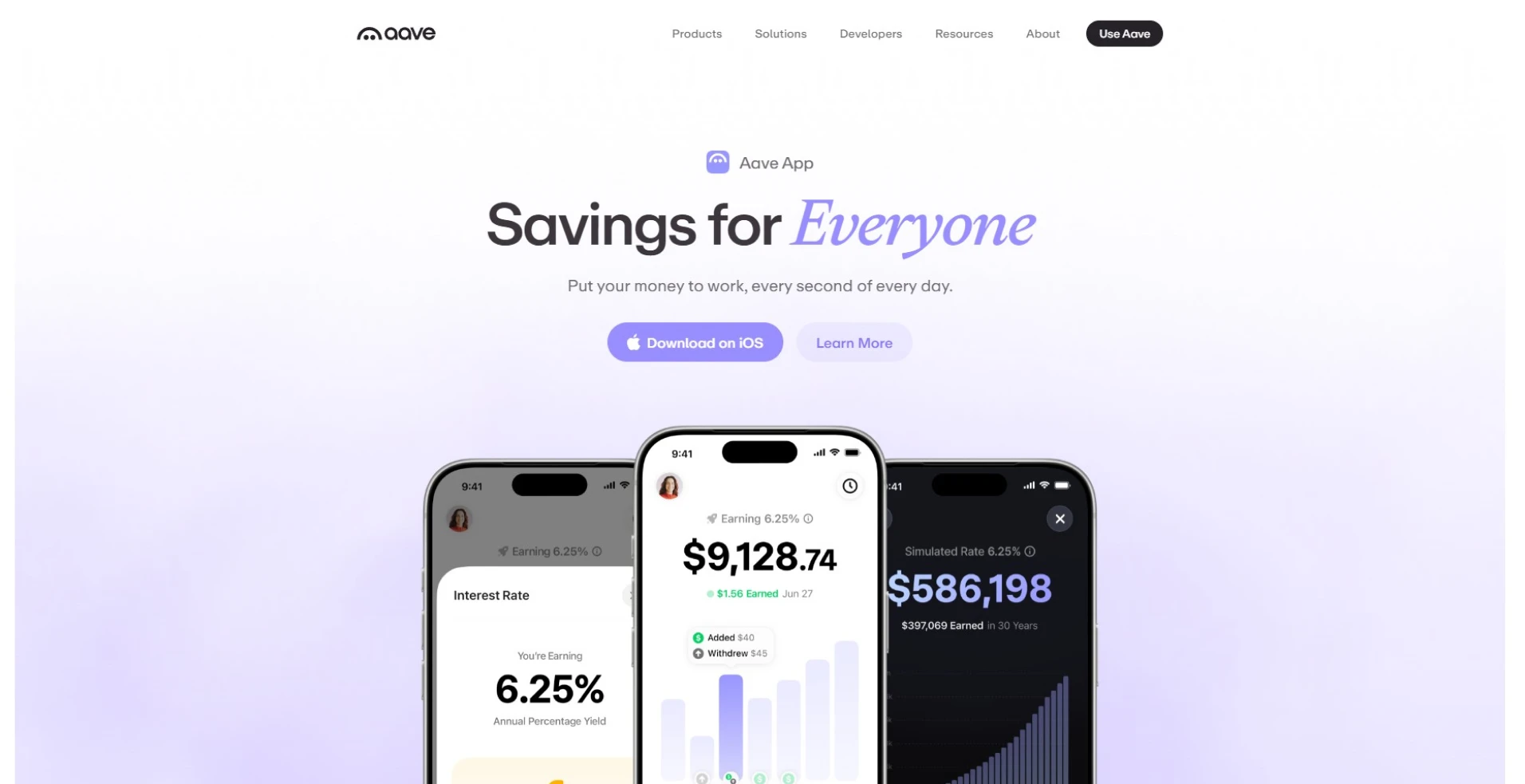

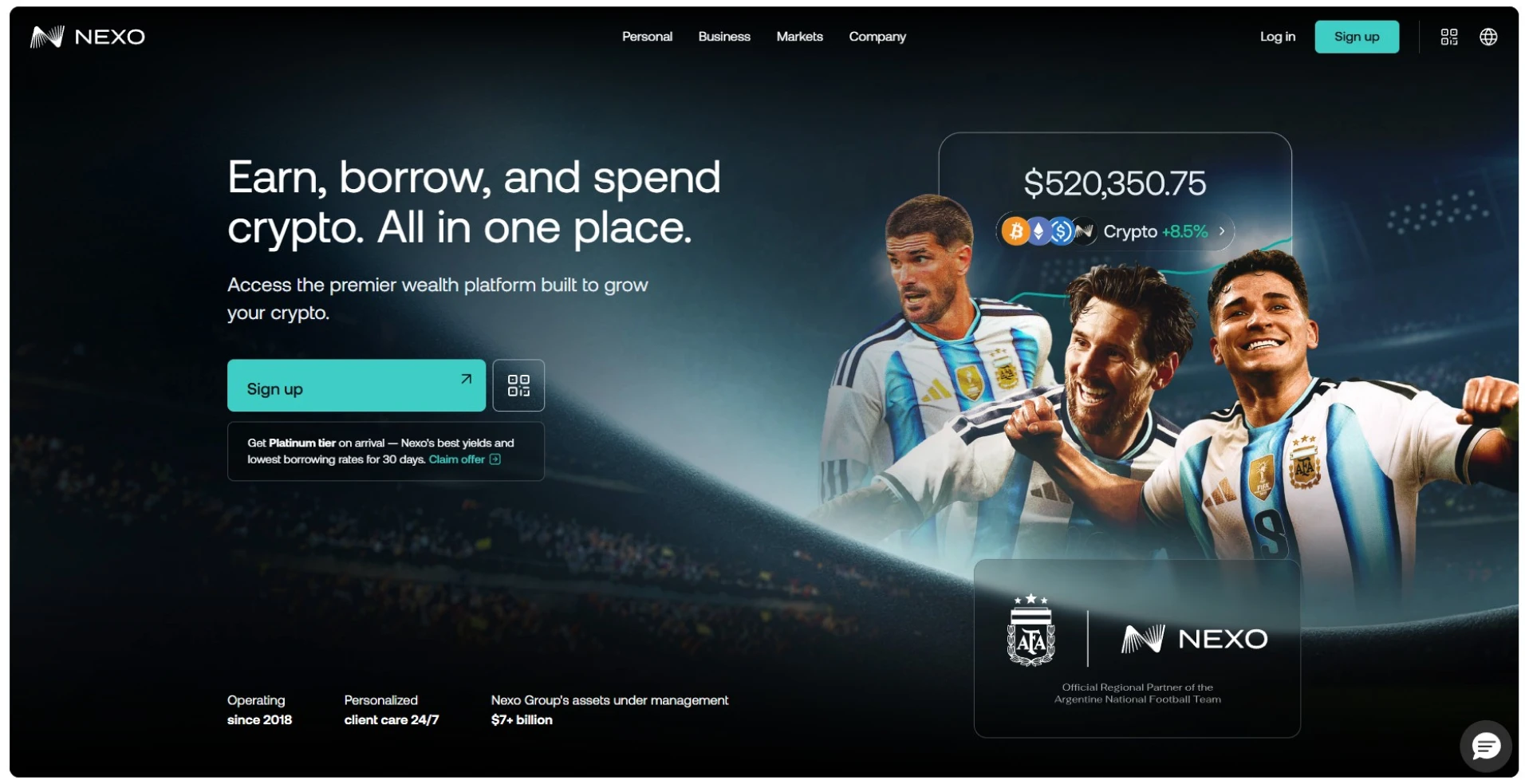

3. Nexo

Best CeFi crypto lending platform, high earn rates with NEXO token benefits.

Nexo is a leading centralised crypto lending platform by assets under management, combining high-yield earn products with instant crypto-backed loans across 65+ supported assets. Its tiered loyalty programme, structured around NEXO token holdings as a percentage of portfolio, provides the clearest fee and rate differentiation of any CeFi lending platform. Top-tier Platinum members access the lowest borrowing rates, with credit lines starting from 1.9%. Earn rates of up to 15% APY, meanwhile, are available on stablecoins for the highest loyalty tier. This structure incentivises long-term platform engagement over single-transaction optimisation.

Nexo’s institutional-grade custody partnerships with providers such as Ledger Vault and Fireblocks provide asset security infrastructure comparable to regulated custodians. The platform operates with a regulatory presence across multiple jurisdictions and holds licences in several markets. Loan terms are flexible, so borrowers can access funds immediately against deposited collateral with no fixed repayment schedule, paying interest only on the outstanding balance. This structure suits both short-term liquidity events and longer-term capital efficiency strategies for crypto-heavy portfolios.

Key stats

- Type: Centralised, custodial

- Supported assets: 65+ cryptocurrencies and fiat currencies

- Borrow APR: From 1.9% (Platinum tier) to standard tiers

- Earn APY: Up to 15% on stablecoins (Platinum tier)

- Collateral: Crypto and fiat, flexible LTV

- KYC: Required

- Custody: Institutional custody via Ledger Vault, Fireblocks

- Strengths: NEXO tier rewards, low-rate credit lines, high APY, regulated custody, instant approval

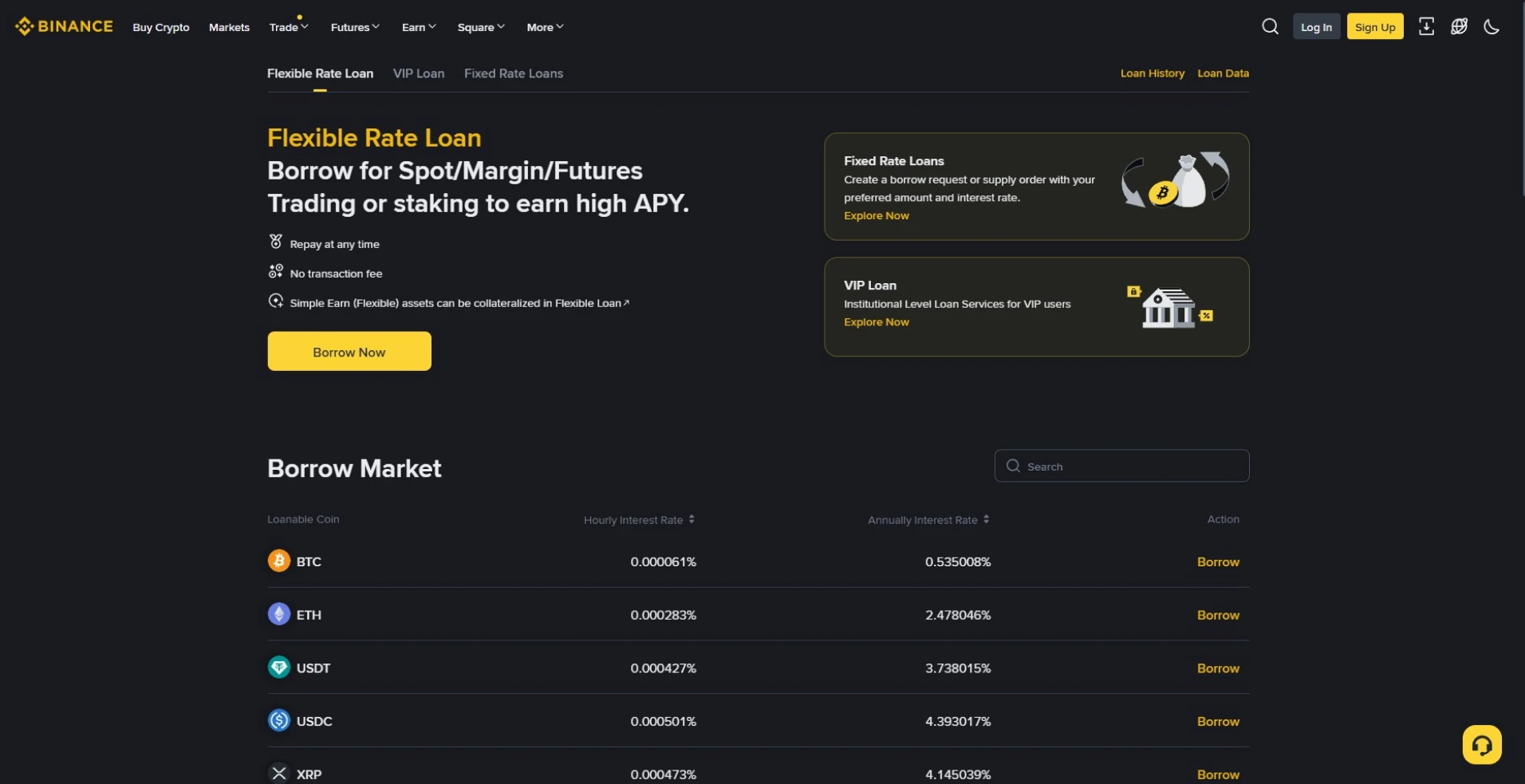

4. Binance Loans

Best crypto lending for Binance users, 100+ collateral assets with flexible terms.

Binance Loans leverages the world’s largest crypto exchange infrastructure to provide crypto-backed lending directly within the Binance ecosystem. Users can borrow against 100+ collateral assets including BTC, ETH, BNB, and a wide range of altcoins. Loan terms range from 7 to 180 days, with loan-to-value ratios up to 65%. The integration with Binance’s spot and futures accounts lets borrowed funds be deployed immediately into trading positions, staking products, or yield strategies without transfer delays. This is a capital efficiency advantage that standalone lending platforms cannot provide.

Binance’s Simple Earn and Flexible Savings products sit alongside Loans within the same account interface, creating a unified experience for users who want both lending and earning from a single platform. Borrowing rates start from 6% APR and vary by asset and term, with BNB holders receiving rate discounts consistent with Binance’s broader fee reduction mechanics. In addition, the platform’s scale provides deep liquidity for large loan positions that smaller CeFi lenders cannot accommodate, and Binance’s proof-of-reserves publication provides ongoing solvency verification.

Key stats

- Type: Centralised, custodial (within Binance)

- Collateral assets: 100+ cryptocurrencies

- Borrow APR: From 6%, varies by asset and term

- Earn APY: Up to 20% (Binance Simple Earn products)

- Loan terms: 7 to 180 days, flexible repayment

- LTV: Up to 65% depending on collateral asset

- KYC: Required (Binance account KYC)

- Strengths: Exchange integration, 100+ collateral, BNB rate discounts, proof of reserves, scale

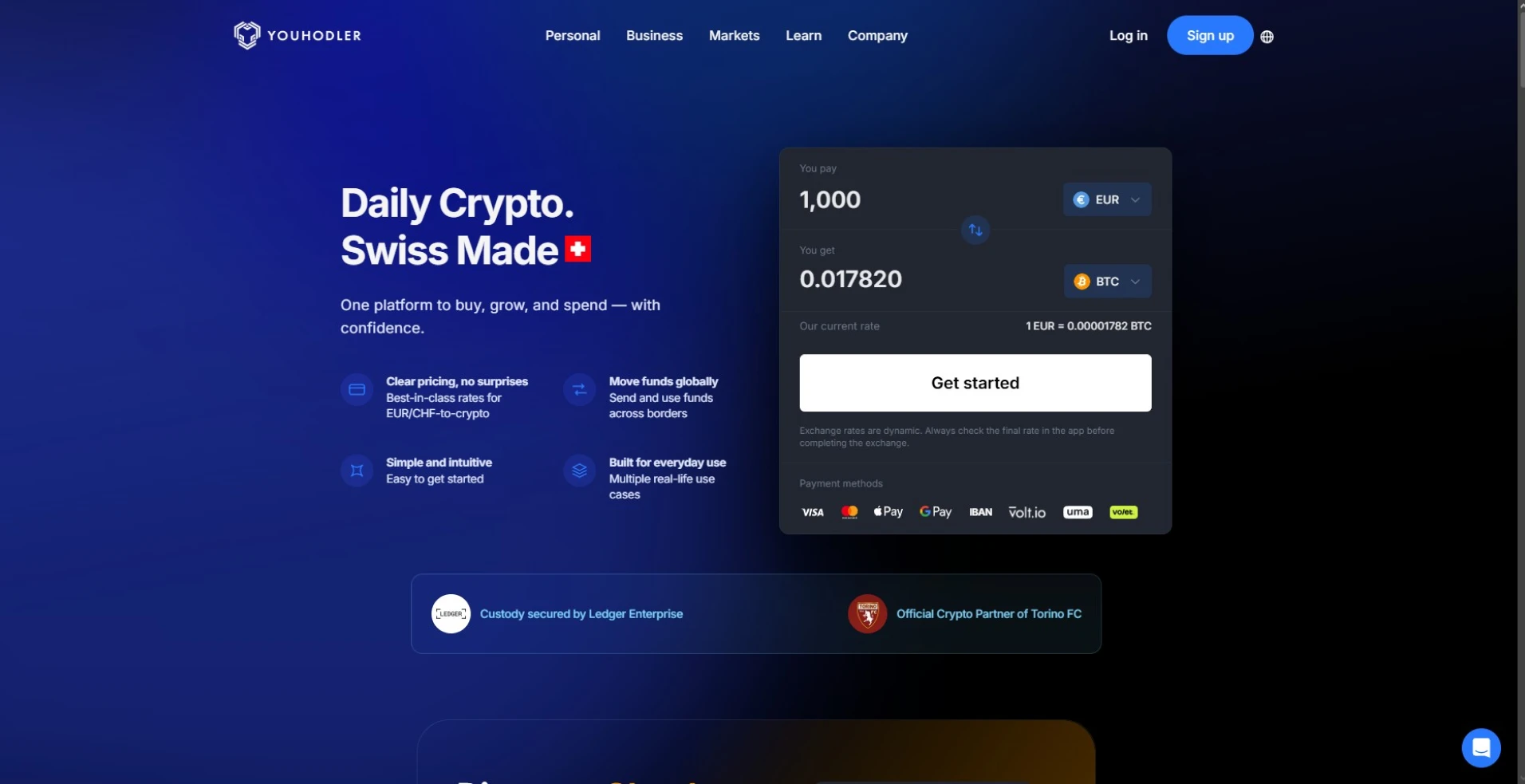

5. YouHodler

Best for high LTV crypto loans, Multi-HODL and earn products for active users.

YouHodler occupies a distinct position in the CeFi lending market through its combination of high loan-to-value ratios and a product suite that extends well beyond standard crypto loans. LTV ratios of up to 97% on BTC-backed loans, among the highest available on any regulated lending platform, let borrowers extract near-full liquidity from crypto positions without selling underlying assets. The platform supports 50+ collateral assets and offers EUR, USD, GBP, and CHF as borrowing currencies, making it particularly accessible to European users seeking fiat liquidity against crypto holdings.

YouHodler’s Multi-HODL product is its most distinctive feature: a leveraged position tool that chains multiple loan-and-buy cycles automatically, letting users build leveraged exposure to BTC, ETH, or other assets without manually managing each cycle. This product effectively functions as a simplified on-platform margin tool for users who want directional exposure without accessing a derivatives exchange. The Savings Accounts offering, meanwhile, earns up to 10.3% APY on stablecoins and selected cryptocurrencies, with weekly interest payments rather than the daily compounding structure used by some competitors.

Key stats

- Type: Centralised, custodial

- Supported assets: 50+ cryptocurrencies; EUR, USD, GBP, CHF loans

- Borrow APR: From 7.9%, varies by asset and LTV

- Earn APY: Up to 10.3% on stablecoins and select assets

- Max LTV: Up to 97% on BTC (highest in class)

- KYC: Required

- Fiat currencies: EUR, USD, GBP, CHF

- Strengths: Ultra-high LTV, Multi-HODL leverage tool, European fiat access, weekly interest payments

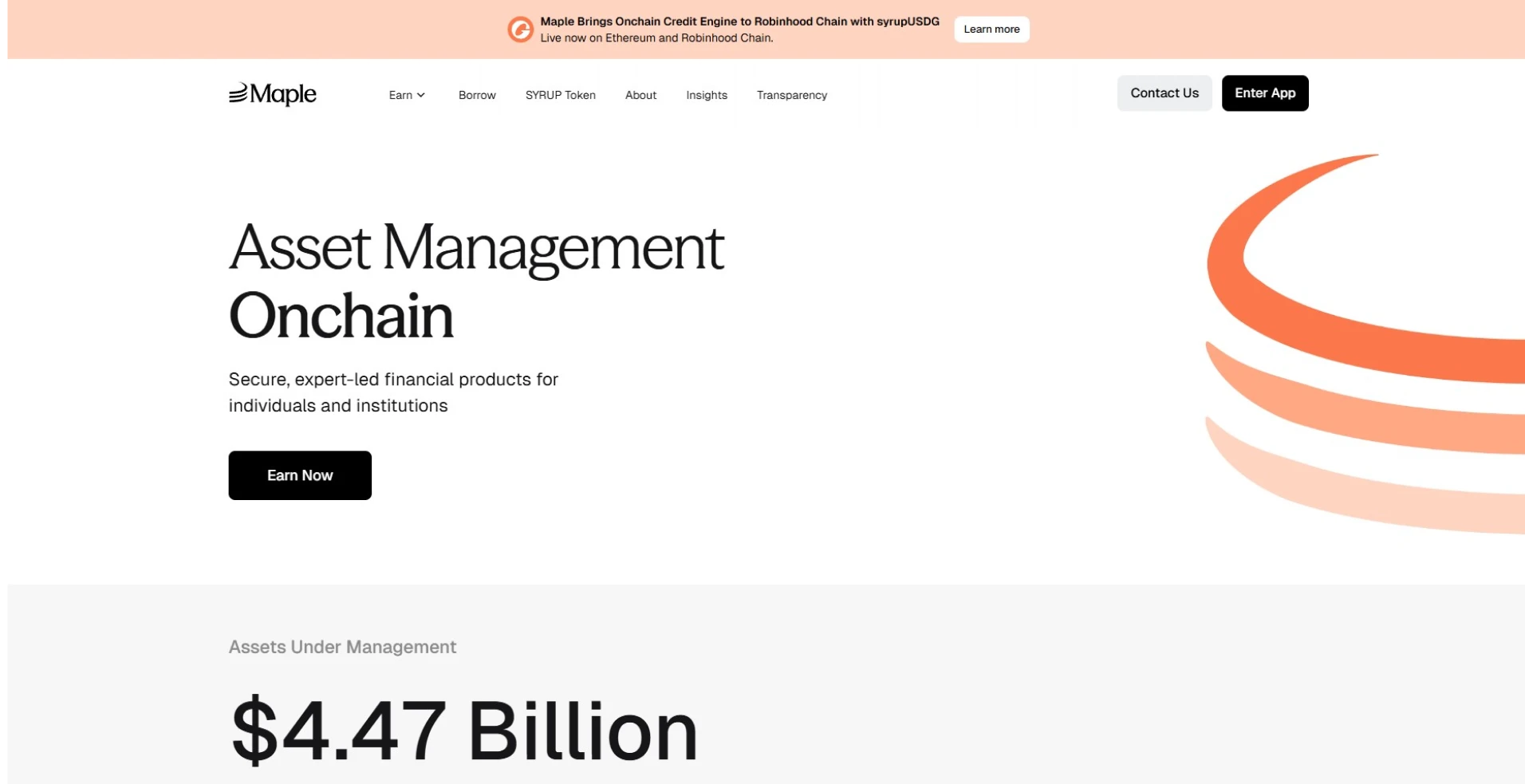

6. Maple Finance

Best institutional crypto lending protocol, undercollateralised pools for verified borrowers.

Maple Finance operates at the intersection of DeFi infrastructure and institutional credit markets, providing undercollateralised lending pools where vetted institutional borrowers can access crypto capital without posting 100%+ collateral. Pool delegates, professional credit managers who conduct due diligence on behalf of liquidity providers, manage each lending pool and set terms for borrower admission, creating an on-chain credit market with real-world underwriting discipline. For institutional lenders seeking higher yields than over-collateralised DeFi protocols can offer, Maple’s credit pools have historically delivered 6–12% APY on USDC. Risk is managed through borrower vetting rather than collateral liquidation.

Maple’s cash management pools serve institutional borrowers including market makers, trading firms, and Web3-native companies that need working capital without liquidating crypto treasury positions. Specifically, the protocol operates on Ethereum and Solana, with pool-level KYB (Know Your Business) requirements that restrict participation to verified entities, a structure that positions it firmly within institutional DeFi rather than retail crypto finance. Notably, Maple’s transparent on-chain loan book lets lenders monitor outstanding positions, repayment schedules, and pool health in real time, which no traditional credit fund can match on auditability.

Key stats

- Type: Hybrid DeFi, institutional, non-custodial

- Borrower type: Institutional, market makers, trading firms, Web3 companies

- Collateral: Undercollateralised, credit-based underwriting

- Earn APY: 6–12% USDC (pool-dependent)

- Supported chains: Ethereum, Solana

- KYC/KYB: Required for all participants (institutional KYB)

- Strengths: Undercollateralised pools, on-chain loan book, institutional credit discipline, real-time auditability

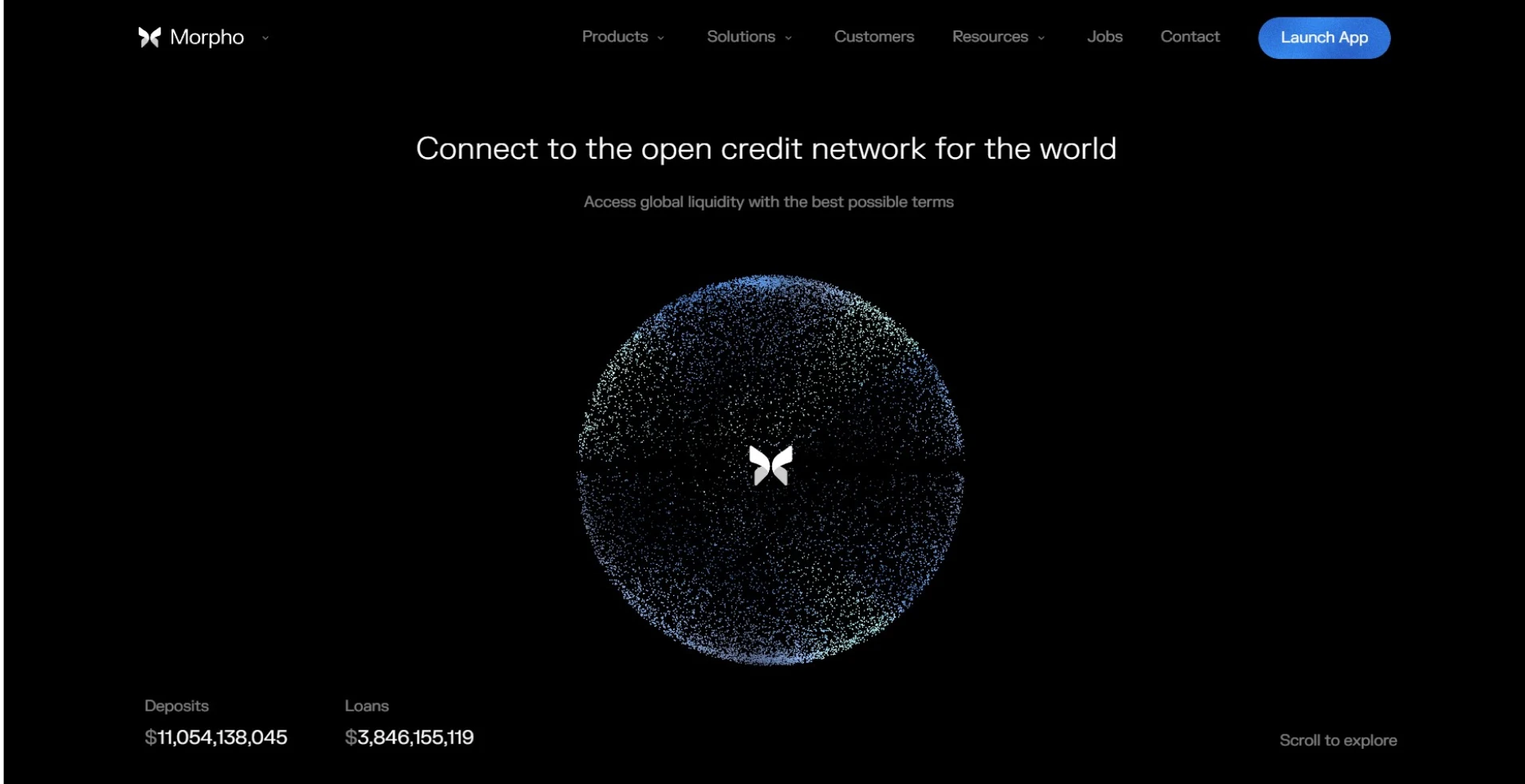

7. Morpho

Best rate-optimised DeFi lending, peer-to-peer matching on top of Aave and Compound.

Morpho introduces a peer-to-peer matching layer on top of existing DeFi lending pools, primarily Aave and Compound. When a direct counterparty match is possible it improves rates for both sides, and it falls back to the underlying pool rate when no match is available. As a result, lenders earn rates between pool supply APY and pool borrow APY, while borrowers pay rates below what they would pay directly on Aave or Compound. Importantly, this architecture requires no new liquidity bootstrapping, since the protocol inherits the security and liquidity of established pools while extracting efficiency gains from the spread between supply and borrow rates.

Morpho Blue, the protocol’s standalone lending primitive launched in 2024, extends the model beyond Aave and Compound by allowing the creation of isolated lending markets for any asset pair with customisable risk parameters. Consequently, this has enabled an explosion of specialised lending markets, including liquid staking token markets, restaking asset markets, and real-world asset collateral markets, that the monolithic pool structure of Aave cannot easily accommodate. For lenders who want Aave-like security with improved yield, or borrowers who want Compound-equivalent access at lower rates, it provides a measurable improvement without requiring trust in a new security model.

Key stats

- Type: Decentralised, non-custodial, built on Aave/Compound

- TVL: $3B+ (Morpho Blue and Morpho Optimisers combined)

- Supported chains: Ethereum, Base, Optimism, Polygon

- Borrow rates: Below Aave/Compound rates via P2P matching

- Earn APY: Above Aave/Compound supply rates via P2P matching

- KYC: None, permissionless

- Strengths: Better rates vs base protocols, inherited security model, Morpho Blue isolated markets, composable

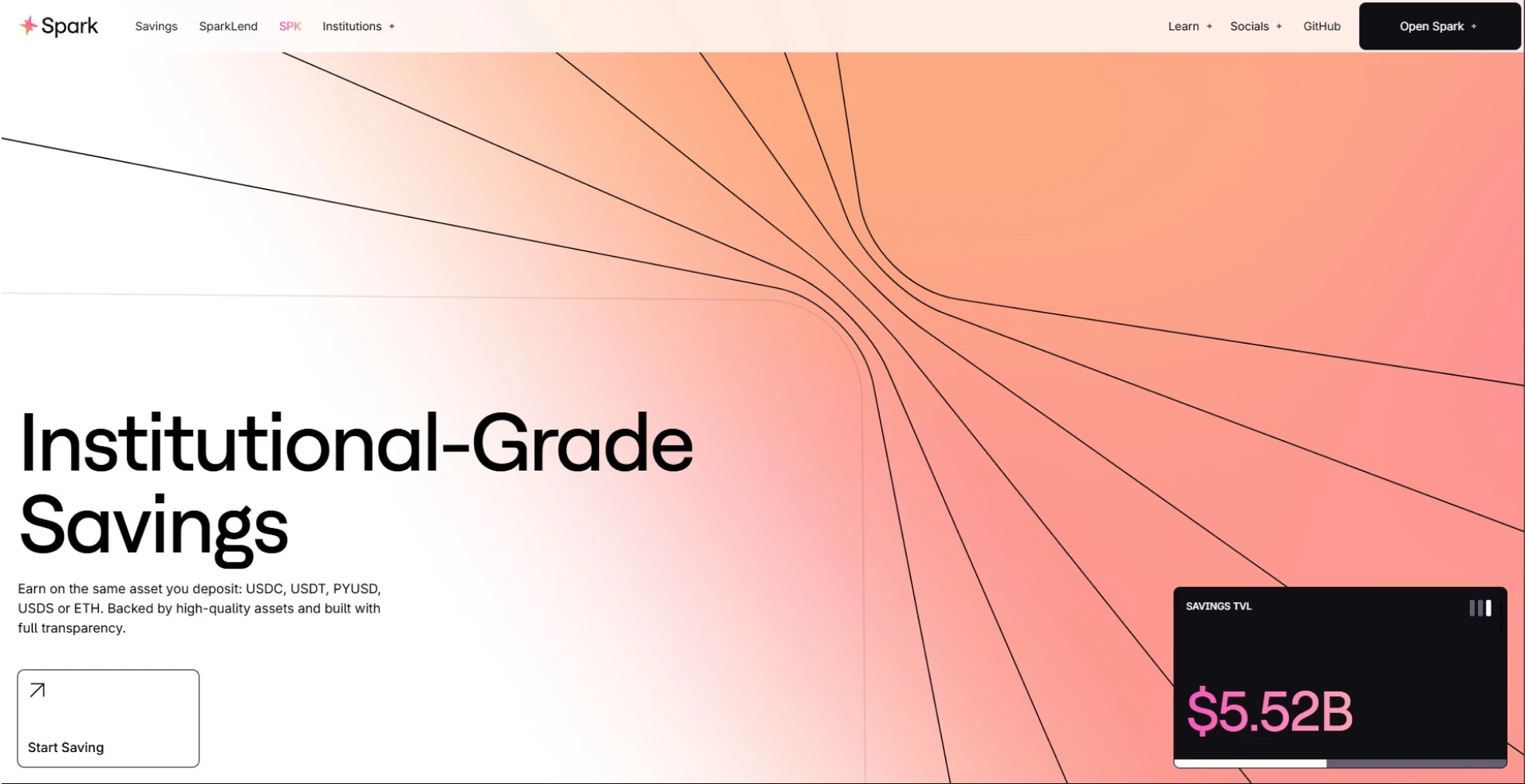

8. Spark Protocol

Best MakerDAO-native lending platform, sDAI savings rate and DAI-centric lending.

Spark Protocol is the official lending frontend of the MakerDAO ecosystem, providing a DAI-centric lending and borrowing experience powered by the same smart contract infrastructure that underpins Maker’s collateral management system. Borrowers can access DAI against ETH, wBTC, and select liquid staking tokens at rates set by MakerDAO governance, typically at or below Aave’s equivalent rates for the same collateral. Lenders, in turn, can deploy into the sDAI (Savings DAI) product, which automatically earns the DAI Savings Rate set by MKR governance. The DAI Savings Rate has been a competitive on-chain yield benchmark, at times exceeding rates available on mainstream CeFi platforms.

Spark’s deep integration with MakerDAO’s balance sheet creates a structural advantage that independent protocols cannot replicate. DAI minted against collateral on Spark is backed by the same over-collateralisation and liquidation infrastructure that has maintained DAI’s peg through every major market stress event since 2019. As a result, for DeFi users who want stablecoin lending exposure within the most battle-tested stablecoin ecosystem on Ethereum, Spark provides the most direct access. Furthermore, the protocol is expanding to support additional collateral types and chains under the Endgame roadmap, which will broaden its addressable market through 2026 and beyond.

Key stats

- Type: Decentralised, MakerDAO-native, non-custodial

- Supported assets: ETH, wBTC, stETH, rETH, DAI (primary borrowing asset)

- Borrow rates: Governed by MakerDAO, competitive with Aave

- Earn APY: sDAI (DAI Savings Rate), dynamically set by governance

- Chains: Ethereum primary; multi-chain expansion underway

- KYC: None, permissionless

- Strengths: MakerDAO backing, sDAI savings rate, battle-tested infrastructure, governance-set rates

9. CoinRabbit

Best no-KYC crypto lending platform, instant loans against 130+ assets.

CoinRabbit provides one of the most accessible centralised crypto lending experiences available in 2026: no KYC, no credit checks, no account registration required beyond a receiving address for loan proceeds. Borrowers send supported crypto collateral to a CoinRabbit address and receive stablecoin or fiat loan proceeds within minutes. No documents are submitted, and no identity is linked to the transaction beyond the on-chain collateral transfer. This model serves users in jurisdictions where conventional lending is inaccessible, privacy-conscious borrowers who prefer minimal data exposure, and situations where speed of access matters more than rate optimisation.

Support for 130+ collateral assets, one of the broadest asset lists in the CeFi lending market, means CoinRabbit can accommodate positions in altcoins that Nexo, YouHodler, and Binance Loans would reject as collateral. Additionally, loan-to-value ratios of up to 70% are available across major assets, with variable borrow rates starting from 10% APR, and the platform also offers a savings product earning up to 15% APY on USDC and USDT. However, the trade-off for the no-KYC model is rate: CoinRabbit’s borrowing costs are higher than KYC-required competitors, and there is no loyalty tier or rate reduction mechanism for larger or repeat borrowers.

Key stats

- Type: Centralised, custodial

- Supported collateral: 130+ cryptocurrencies

- Borrow APR: From 10%, higher than KYC-required peers

- Earn APY: Up to 15% on USDC and USDT

- Max LTV: Up to 70%

- KYC: None required, fully anonymous access

- Loan speed: Minutes, no registration, no documents

- Strengths: No-KYC, 130+ collateral assets, instant access, broad jurisdiction support

10. Clearpool

![]()

Best permissioned institutional lending pool, single-borrower DeFi credit markets.

Clearpool operates single-borrower permissioned lending pools where institutional entities, including crypto trading firms, fintechs, and Web3 companies, borrow directly from on-chain liquidity providers under a vetted, KYB-gated framework. This differs from Maple Finance’s pool delegate model, where a credit manager intermediates between lenders and a borrower pool. By contrast, Clearpool pools are dedicated to a single named borrower, giving lenders full transparency over exactly who is holding their capital and under what terms. Interest rates are dynamic, adjusting based on pool utilisation, which creates a market mechanism for pricing institutional credit risk on-chain.

Clearpool’s Ozean network, its institutional credit layer, has expanded the protocol’s reach into regulated institutional lending with additional compliance infrastructure, targeting asset managers and fintechs that require a permissioned environment aligned with emerging DeFi regulatory frameworks. In addition, lenders earn CPOOL token rewards on top of base interest, improving effective yield on open pools. Ultimately, for institutional lenders who want the yield premium of undercollateralised credit with on-chain verifiability and named counterparty transparency, Clearpool provides a level of borrower accountability that anonymous pool structures cannot match.

Key stats

- Type: Hybrid DeFi, permissioned institutional, non-custodial

- Borrower type: Single named institutional borrowers per pool

- Collateral: Unsecured, credit-based, KYB-verified borrowers

- Earn APY: 5–15%+ (base rate + CPOOL rewards)

- Supported chains: Ethereum, Polygon, Optimism, Mantle

- KYC/KYB: Required for borrowers; lenders have permissioned access

- Strengths: Named borrower transparency, dynamic rate pricing, CPOOL rewards, Ozean institutional layer

How to Choose the Right Crypto Lending Platform in 2026

No single lending platform is optimal for every user. The right choice depends on whether you are borrowing or earning, your tolerance for custodial risk, the collateral assets you hold, and whether you need fiat loan proceeds or are comfortable receiving stablecoins.

Use Case

- Non-custodial borrowing with maximum capital efficiency: Aave on Ethereum or Arbitrum provides the deepest liquidity, the broadest asset support, and full on-chain position transparency with no counterparty risk.

- High-yield stablecoin earnings with CeFi convenience: Nexo’s Platinum tier offers up to 15% APY on USDC and USDT with weekly interest payments and institutional custody infrastructure.

- Institutional undercollateralised credit: Maple Finance provides vetted institutional borrowers with on-chain capital access and lenders with above-DeFi yields backed by credit underwriting rather than collateral.

- Better rates on existing DeFi positions: Morpho improves on Aave and Compound rates for the same assets and collateral without requiring trust in a new security model.

- Instant no-KYC liquidity: CoinRabbit provides the fastest, most anonymous access to crypto-backed loans across 130+ collateral assets with no identity verification.

Collateral Asset

- BTC, ETH, top 20 assets: All platforms on this list accept major assets; DeFi protocols offer the most transparent liquidation mechanics while CeFi platforms provide fiat loan proceeds.

- Long-tail altcoins: CoinRabbit (130+ assets) and Binance Loans (100+ assets) support the broadest collateral range for non-standard assets.

- Liquid staking tokens (stETH, rETH): Aave, Spark, and Morpho have native support for LSTs with efficiency mode pricing that improves borrowing capacity versus standard collateral.

- Institutional treasury assets: Maple Finance and Clearpool serve institutional borrowers with credit-based access that over-collateralised models cannot accommodate.

Regulatory and Privacy Requirements

- Full KYC with regulated custody: Nexo and Binance Loans provide the strongest compliance frameworks for users who require regulated counterparties.

- No-KYC with immediate access: CoinRabbit and DeFi protocols (Aave, Compound, Morpho, Spark) require no identity verification, and DeFi protocols additionally require no account creation of any kind.

- European fiat loans: YouHodler is the strongest option for EUR, GBP, and CHF loan proceeds against crypto collateral, with the highest LTV ratios in the regulated CeFi segment.

- US-accessible DeFi: Aave, Compound, Morpho, and Spark are accessible to US users as permissionless protocols; most CeFi platforms restrict US users due to regulatory requirements.

How Cryptic Helps Web3 Brands Grow

Cryptic is a crypto marketing agency with offices in Amsterdam, Dubai, London, and Riyadh, founded in 2020 and a verified Circle Alliance Partner. We have worked with clients including Binance, Bybit, OKX, Algorand and Canton. For DeFi protocols and lending platforms, we build the marketing infrastructure that creates market presence, from user acquisition and protocol integration announcements to authority-building PR and content that earns discovery long after launch. In a market rebuilt on transparency and trust, clear positioning is how a lending brand turns a protocol into an audience.

Book a strategy call with Cryptic →

Frequently Asked Questions

What is the best crypto lending platform in 2026?

Aave leads for non-custodial DeFi lending with the deepest multi-chain liquidity and full on-chain transparency. Nexo leads for CeFi lending with high earn rates, institutional custody, and the most structured loyalty rewards programme. The right answer depends primarily on whether you prioritise non-custodial security or fiat currency access and CeFi convenience.

Is crypto lending safe after the 2022 CeFi collapses?

DeFi lending protocols such as Aave, Compound, and Morpho were not materially affected by the 2022 CeFi collapses, since smart contract-based lending continued operating normally throughout. CeFi platform risk has reduced for surviving regulated operators like Nexo and Binance Loans, which have published proof-of-reserves and operate under regulatory frameworks. The risk remains present for any platform that custodies user assets, so due diligence on reserves, insurance, and regulatory standing is essential.

What is the difference between DeFi and CeFi crypto lending?

DeFi lending uses audited smart contracts to manage collateral, rates, and liquidations on-chain with no central custodian, so users retain control of assets at all times and positions are transparently verifiable by anyone. CeFi lending uses a centralised platform that custodies your collateral and manages loans through their own systems, typically offering fiat loan proceeds, fixed rates, and a more familiar interface in exchange for counterparty risk.

What LTV ratio can I get on a crypto loan?

LTV ratios vary significantly by platform and collateral asset. YouHodler offers the highest CeFi LTV at up to 97% on BTC. Nexo and Binance Loans offer up to 65% or more depending on tier and asset. DeFi protocols vary by collateral: ETH on Aave supports up to 80% LTV, while more volatile assets have lower ceilings. The liquidation threshold is always set below the maximum LTV, so maintaining a buffer is essential to avoid automatic liquidation during price drops.

Do I need KYC to use a crypto lending platform?

DeFi protocols such as Aave, Compound, Morpho, and Spark require no KYC, since positions are opened directly from a wallet with no registration. CoinRabbit is the leading no-KYC CeFi option. All other CeFi platforms on this list (Nexo, Binance Loans, YouHodler, Maple, Clearpool) require full KYC or KYB. Institutional platforms like Maple and Clearpool require business-level verification for all participants.

What are typical crypto lending interest rates in 2026?

Borrowing rates range from around 1.9% (Nexo top tier on select assets) to over 13% on CeFi platforms, and from 1% to 10%+ on DeFi protocols depending on pool utilisation. Earn rates range from 1–6% on DeFi lending pools such as Aave and Compound to up to 15% on CeFi stablecoin savings at Nexo’s Platinum tier. Always compare the effective rate at your actual tier or pool utilisation level, since headline rates typically reflect best-case conditions.